- Trading

- Trading

- Markets

- Markets

- Accounts

- Accounts

- Platforms & tools

- Platforms & tools

- Platforms

- Platforms

- Premium trading tools

- Premium trading tools

- Education

- Education

- Resources

- Resources

- Courses

- Courses

- Help & support

- Help & support

- About

- About

- Client support

- Trading

- Trading

- Markets

- Markets

- Accounts

- Accounts

- Platforms & tools

- Platforms & tools

- Platforms

- Platforms

- Premium trading tools

- Premium trading tools

- Education

- Education

- Resources

- Resources

- Courses

- Courses

- Help & support

- Help & support

- About

- About

- Client support

News & Analysis

News & AnalysisAsian markets looking to open strongly as big tech pushes US markets higher ahead of CPI

13 June 2023US markets rallied strongly again to start the week with lower yields, on the back of hopes of a Fed pause this week, saw big tech surge and the Nasdaq (+1.53%) lead major indices to print fresh YTD highs.

Another day, another up day for Tesla (TSLA) with its stock price rising for the 12th straight day – the longest winning streak in the company’s history. Apple (AAPL) also hit a milestone, breaking out to all-time highs after rallying 1.56% during the session.

Despite a positive session in equities, the VIX index surged, as traders started to hedge their bets ahead of what could potentially be a tumultuous week with CPI, FOMC, ECB , BoJ and Quad-Witch OpEx all on the calendar.

FX Markets

USD tracked Treasury yields in a choppy, but ultimately positive session. An early session sell-off reversed late in the day as yields whipsawed ahead of today’s CPI figure. DXY hit a peak of 103.75 and held above the 7th of June low of 103.64 at the tail end of the session.

EUR was slightly higher against the USD and was the G7 outperformer, EURUSD hit a high of 1.0790 early in the session before pulling back to close at 1.0750, the move lower being led by a rally in US yields.

AUD and NZD were mixed. AUDUSD saw a high of 0.6773 early on before retreating to slightly firmer levels around 0.6750 as gains in the USD pushed the pair lower from its highs, lower metal prices also weighed on AUD. NZDUSD was flat, falling from earlier highs of 0.6152 to lows of 0.6107 but found support just above 0.6100. AUDNZD rose from lows of 1.10 to highs of 1.1039.

Commodities

Gold was down modestly, following the USD in a choppy sideways session, XAUUSD continuing to trade within its range between 1983 – 1938 USD an ounce. Oil prices tumbled in Mondays session, not helped by Goldman Sachs slashing their year-end forecast, USOUSD hitting a $66 handle, its lowest close since March.

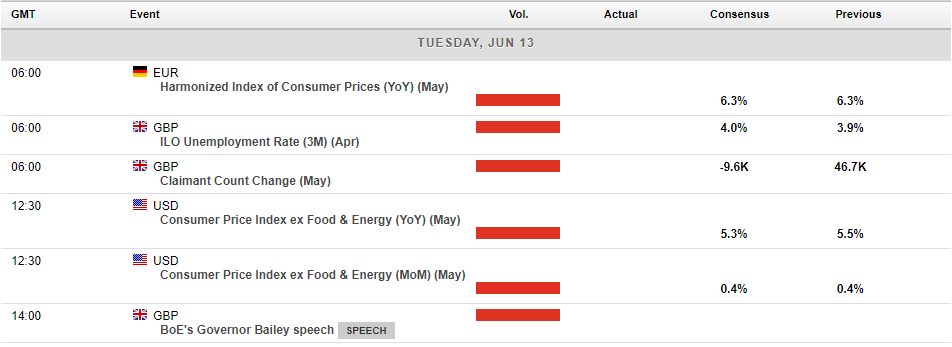

In economic announcements today, main risk events kick off today with US CPI for May being released. Inflation is predicted to continue to slow, but with a pivotal FOMC meeting on Thursday with the market split as to whether another hike is coming or not, any miss in this figure (high or low) should see some rapid repricing of FX and equity markets.

Disclaimer: Articles are from GO Markets analysts and contributors and are based on their independent analysis or personal experiences. Views, opinions or trading styles expressed are their own, and should not be taken as either representative of or shared by GO Markets. Advice, if any, is of a ‘general’ nature and not based on your personal objectives, financial situation or needs. Consider how appropriate the advice, if any, is to your objectives, financial situation and needs, before acting on the advice.

Next Article

Wall St rallies on softer CPI ahead of FOMC, USD down, Yields up

Another day, another stock rally on Wall St in Tuesday’s session with a softer than expected headline CPI print seeing US rate hike odds completely evaporate before today’s pivotal FOMC meeting. Small caps led the way with the Russell 2000 rising 1.23%, and another record for TSLA, surging 41% in the last 13 green trading sessions. U...

June 14, 2023Read More >Previous Article

Wall St rally sees S&P 500 enters technical bull market – VIX dumps, Gold pumps

A tech led rally saw the S&P 500 index enter a technical bull market after rallying 20% from the October 2022 lows, a big miss on unemployment cla...

June 9, 2023Read More >

- Trading

- Trading

- Trading

- Markets

- Markets

- Accounts

- Accounts

- Platforms & tools

- Platforms & tools

- Platforms

- Platforms

- Premium trading tools

- Premium trading tools

- Education

- Education

- Resources

- Resources

- Courses

- Courses

- Help & support

- Help & support

- About

- About

- Client support